In this video blog series on insurance recovery law, top insurance recovery lawyers address some of the most pressing and important insurance coverage issues faced by corporate policyholders today.

Here, Brian Friel addresses some of the complexities and nuances of insurance recovery law. It takes decades of full immersion into this area of practice to understand how best to handle complex corporate insurance claims. This is not an area of law that can be easily navigated by non-insurance lawyers. Corporations with insurance claims are best served by working with a team of attorneys who sole focus is insurance recovery law.

Please join Brian in this video as he discusses further the benefits of Experience and Focus.

In this video blog series on insurance recovery law, top insurance recovery lawyers address some of the most pressing and important insurance coverage issues faced by corporate policyholders today.

We believe that the best way to introduce our new video blog series is to start by sharing some of our thoughts on the factors that differentiate great insurance recovery lawyers and law firms, from all of the others who practice in this specialized area of law. In this video our Managing Partner, Brian Friel, explains the necessity of focusing on one specific area of law, and why this kind of sole focus in a law firm helps clients maximize the value of their corporate insurance assets.

Please take a moment to watch Brian talk about what sets Miller Friel apart from other insurance recovery practices.

Miller Friel, PLLCis a specialized insurance recovery law firm whose sole purpose is to help corporate clients maximize their insurance coverage. Our Focusof exclusively representing policyholders, combined with our extensive Experiencein the area of insurance recovery law, leads to greater efficiency, lower costs and better Results. Further discussion and analysis of insurance coverage issues impacting policyholders can be found in our Miller Friel Insurance Coverage Blog and our 7 Tips for Maximizing Coverage series.

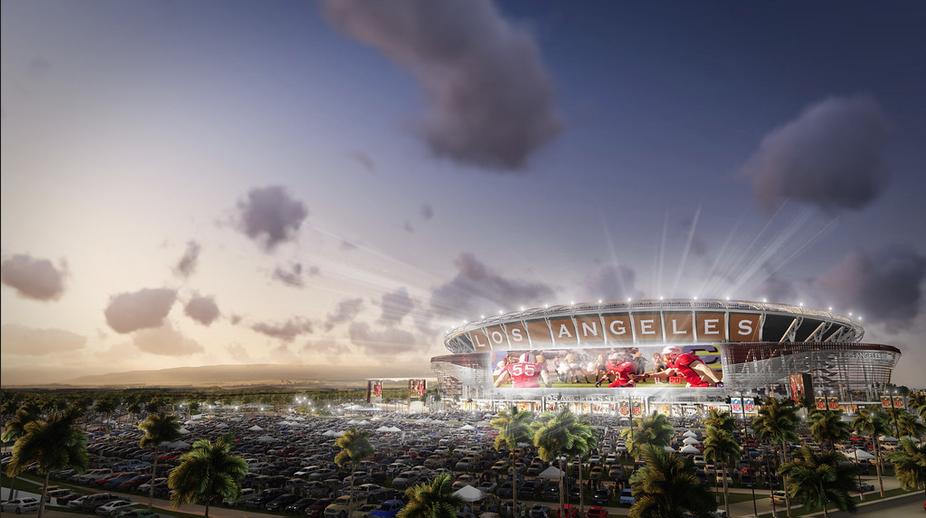

One Possible Design for the New Los Angeles Football Stadium.

Just recently, the City of Carson, California, about 10 miles south of downtown Los Angeles, approved the redevelopment of a former landfill site into a 80,000 seat football stadium, which one day may be the home stadium of the San Diego Chargers and the Oakland Raiders. There is enormous support for this project, from local and state authorities, the NFL, and the millions of football fans who want to see professional football return to the nation’s second largest city. This two-team stadium is expected to be the most expensive sports arena ever built, with some estimates putting the price tag north of $1.5 billion.

Miller Friel played an integral part in this transformative transaction by providing legal and strategic advice to Tetra Tech, Inc.. Tetra Tech, one of the nation’s leading engineering and environmental companies, is responsible for the remediation of the site. Miller Friel assisted Tetra Tech in securing funding under its environmental insurance policy, providing coverage for, among other things, environmental remediation and related operations and maintenance costs for work performed by Tetra Tech over the past eight years. We also provided assistance to ensure that there was continuous environmental insurance coverage for the property, which was recently transferred to new owners. Securing insurance funding was particularly important here given the extraordinary costs and environmental complexities associated with the site and its redevelopment.

“This project is one of the largest and most important redevelopment projects in the United States, and Miller Friel is honored to work with Tetra Tech and its team of professional engineers, architects and designers to ensure the best possible result, says Brian Friel, MIller Friel’s Co-Founder and Managing Partner. According to Brian, “this project is a reflection of the quality of work that Miller Friel does, the national scope of our practice, and the value-added services we provide.”

We hope to report back in a few years with a photo of the Miller Friel legal team on the sidelines of a Chargers-Raiders game at the new Los Angeles Stadium in Carson, California. Stay tuned.

Miller Friel, PLLC is a specialized insurance coverage law firm whose sole purpose is to help corporate clients maximize their insurance coverage. Our Focus of exclusively representing policyholders, combined with our extensive Experience in the area of insurance law, leads to greater efficiency, lower costs and better Results. Further discussion and analysis of insurance coverage issues impacting policyholders can be found in our Miller Friel Insurance Coverage Blog and our 7 Tips for Maximizing Coverage series. For additional information about this post, please call 202-760-3160.

Providing insurers with timely notice of claims is probably the most basic of coverage issues. Think of proper notice as the “Go” box in the board game Monopoly – you can’t get around the board to secure boardwalk hotels or bags of money until you get past “Go.” Claims notice works the same way. A policyholder can obtain and pay for the best insurance policies available, whether General Liability, Property, Directors & Officers, Errors and Omissions, Crime, etc., but the insurer may deny a claim because the policyholder provided notice one month or even one week too late. Sometimes notice is late because of an oversight or neglect on the part of a policyholder, but more often than not, notice is late because of unsuspected traps, particularly those contained in claims made insurance policies. As a recent case illustrates, these traps can be difficult to navigate. Ashland Hospital Corp. v. RLI Ins. Co., Civil Action No.: 13-143-DLB-EBA (EDKY, Northern Div. March 17, 2015).

Hospitals and Health Care Providers are Particularly Vulnerable to Governmental Investigations

In Ashland, Ashland Hospital purchased a $15 million primary D&O liability policy from Darwin National Assurance Company and a $10 million excess D&O liability policy from RLI Insurance Corporation, covering the period October 1, 2010 to October 1, 2011. Both policies are claims-made, which obligated Ashland Hospital to provide notice of claim as soon as practicable but no later than 90 days following expiration of the policy. In addition, the excess policy issued by RLI required Ashland Hospital to provide notice no later than 30 days after: (i) it provides notice to the underlying policy (Darwin), (ii) the alteration or cancellation of the Darwin policy, and (iii) the exhaustion of Darwin’s policy limits.

The facts here are fairly straightforward. On July 25, 2011, the United States Department of Justice issued a subpoena to Ashland Hospital as part of a Health Insurance Portability and Accountability Act (HIPPA) investigation, seeking emails, medical records, insurance billings, medical malpractice claims, and employment contracts related to nine doctors associated with two cardiology groups. Ashland Hospital ultimately agreed to pay $40.9 million to resolve allegations that it billed federal health programs for heart procedures that patients did not medically need. Ashland Hospital notified the primary insurer (Darwin) of the HIPPA investigation on December 30, 2011, 89 days after the policy expired. Darwin accepted coverage and ultimately paid its full $15 million limit. However, Ashland Hospital did not give RLI notice of the HIPPA investigation until June 29, 2012. Two years later, in 2014, Ashland Hospital notified RLI that Darwin had exhausted its underlying limits one week earlier. RLI denied coverage for late notice because Ashland failed to give RLI notice within 30 days of giving notice to Darwin and within the policy period.

Ashland Hospital filed suit against RLI, asserting claims for breach of contract and bad faith. Ashland Hospital contended that it complied with RLI’s notice provision because it timely notified RLI that Darwin’s underlying limits were exhausted and, even if its notice was late, RLI was not prejudiced because the claim had been covered by Darwin up until that point. The federal district court rejected these arguments, holding that (i) Ashland Hospital was required to comply with all of RLI’s 30-day notice requirements, not just one of them, and (ii) under Kentucky law, notice is a condition precedent in claims-made policies, and thus, an insurer need not be prejudiced by late notice to disclaim coverage.

Here is the sad reality of this case — a policyholder hospital forfeited $10 million in excess limits because of its failure to read or properly understand the separate notice requirements set forth in the excess policy. Likewise, it appears that the hospital or its counsel may have been confused, at least initially, as to whether the initial HIPPA-related DOJ subpoenas were even a “claim” as defined in the policies because those subpoenas were directed at two unaffiliated cardiology groups and a group of doctors, not Ashland Hospital. It was these mistakes, or some combination of them, that ultimately led to Ashland Hospital nearly blowing its notice obligation under the primary policy (one day remaining on the 90-day grace period) and completely blowing its 30-day notice obligations under the excess policies. These mistakes cost the hospital $10 million, a payment which the excess insurer would have undisputedly paid if the hospital understood its notice obligations under its entire D&O insurance program.

In Ashland, an excess insurer escaped liability based on a policy technicality. If competent coverage counsel was retained at the beginning of the HIPPA investigation and had a chance to review the subpoenas and the hospital’s D&O policies, Ashland Hospital would have received an additional $10 million in insurance money.

Miller Friel, PLLC is a specialized insurance coverage law firm whose sole purpose is to help corporate clients maximize their insurance coverage. Our Focus of exclusively representing policyholders, combined with our extensive Experience in the area of insurance law, leads to greater efficiency, lower costs and better Results. Further discussion and analysis of insurance coverage issues impacting policyholders can be found in our Miller Friel Insurance Coverage Blog and our 7 Tips for Maximizing Coverage series. For additional information about this post, please email or call Brian Friel (FrielB@MillerFriel.com, 202-760-3162).

As part of our ongoing efforts to be the leading corporate policyholder-only insurance recovery law firm in the country, Miller Friel, PLLC is please to announce that it has opened an office in New York City.

Brian Friel, co-founder and managing partner of Miller Friel stated, “because many of our banking, private equity and financial services clients are headquartered in New York City, it became imperative to have a physical presence in the city.” In addition to financial institutions, Miller Friel also provides insurance recovery services to a series of other companies located in New York, including a major educational institution, a regional transportation agency, and a leading life sciences company.

Mr. Friel, admitted to practice in New York, New Jersey and Washington, DC, will be Miller Friel’s resident partner in New York City, splitting his time between New York and Miller Friel’s other offices in Morristown, New Jersey and Washington, DC.

Miller Friel’s New York City office is located in Midtown at 373 Park Avenue South.

Miller Friel, PLLC is a specialized insurance coverage law firm whose sole purpose is to help corporate clients maximize their insurance coverage. Our Focus of exclusively representing policyholders, combined with our extensive Experience in the area of insurance law, leads to greater efficiency, lower costs and better Results. Further discussion and analysis of insurance coverage issues impacting policyholders can be found in our Miller Friel Insurance Coverage Blog and our 7 Tips for Maximizing Coverage series. For additional information about this post, please email or call Brian Friel (FrielB@MillerFriel.com, 212-203-6750).

A recent Wall Street Journal article, “Big Law Firm Mergers Questioned,” raises some important issues to consider when hiring coverage counsel. As noted in the article, “[l]arge companies tend to use a mix of firms for their legal work, ranging from small boutiques to name-brand Wall Street firms.” Although the article does not expressly address the hiring of insurance coverage counsel, it raises some important considerations.

As stated by John Schultz, General Counsel of Hewlett-Packard Co., “when I talk to my colleagues, we are all still fairly much aligned on the idea that we hire lawyers, not law firms.” The consensus opinion is that lawyer quality matters far more than overall law firm size and geographic reach. Although efficiencies may be achieved by large law firms in situations where a company is defending lawsuits in multiple jurisdictions, quality and reputation of the individual lawyers matters most. Continue reading →